The World of Investing Is about to Change!

By Leland Hevner, President of the National Association of Online Investors (NAOI)

September, 2018

click to enlarge

The world of investing today is not responsive to the needs of the individual investor. Why? Because it is stuck in the past. We have been taught for decades that the only way to invest is by using Modern Portfolio Theory (MPT), an approach to portfolio design introduced in 1952 that creates portfolios to match each investor's risk tolerance level using asset allocation techniques. While markets have changed significantly since the 1950's, MPT has barely changed at all and the portfolios it creates neither enable investors to capture the wealth creation potential of modern markets nor to protect them from market crashes. It is time for fundamental change.

On this Web page you will see what the needed change looks like in the form of Dynamic Investment Theory (DIT) and the Dynamic Investments (DIs) that the theory creates. This is the approach to investing that IS responsive to investor needs and that will finally enable the financial world to evolve as it must to adapt to 21st century markets. Here you will get just a quick glance into the future of investing.

The NAOI and the Study

click for more information about Leland hevner

Allow me to introduce myself as Leland Hevner, President of the National Association of Online Investors. I founded the NAOI in 1997 to empower individuals to invest with confidence and success via education and the use of online resources. Thousands of individuals have taken our personal investing courses, attended our college classes on personal investing and/or read our published books.

From the start, I taught industry standard MPT methods to design portfolios. But in 2008 when the stock market crashed and MPT portfolios crashed with it, I stopped all education activities. I could no longer, in good faith, teach MPT methods that put the savings of my students at risk. I saw that more than education was needed to empower investors, also needed was innovation. I saw that MPT needed to be either modified or replaced to enable individuals to take full advantage of market wealth generation potential.

At that point I refocused NAOI resources on finding a better, more effective approach to investing.

The Search for a Better Approach to Investing

We started our study effort with the firm belief that the future of investing will not be defined in the boardrooms financial corporations or in the halls of academia. It will be defined by the investing public, the users of investment products. Therefore our research effort started by understanding the needs of the individual investor. Fortunately the NAOI is perfectly positioned to do so as our members represent a comprehensive cross section of the individual investor market. Based on surveys and interviews we defined their goals to include these: a simpler investing process, higher returns with lower risk, protection of wealth from market crashes and less dependence on financial professionals.

We immediately saw that these goals could not be met by modifying MPT. So we started with a blank slate, as if MPT never existed. Our design goals focused on increasing the use of scientific methods in the investing process and replacing the use of subjective judgments for making investing decisions and replacing them with decisions based on objective observations of empirical market data. By doing so we hoped to eliminate, or at least mitigate, the massive risk factor introduced to the process by human judgments.

Extensive research showed us that we could meet these design goals by taking advantage of our observation that the prices of assets and markets segments are cyclical, they move up and down over time. We also observed that different asset classes and different market segments move up and down at different times as illustrated in the simple chart just above. This led us to the premise that at all times, in any economic condition, there exist positive returns potential somewhere in the equities market . Our task than became to design an investment vehicle that could capture these returns. We met this goal with the development of NAOI Dynamic Investments that are discussed next.

The Dynamic Investment Components

The Dynamic Investment structure is remarkably simple and effective. A DI is a derivative investment vehicle that combines Exchange Traded Funds (ETFs) – or Mutual Funds - in an intelligent, dynamic structure. It has three design elements as shown in the nearby diagram. The Dynamic ETF Pool is where designers place ETFs that track the asset classes and/or market areas where they want the DI to search for positive price trends. The other two variables are a very simple Trend Indicator and a Review Period.

At periodic Review events, typically occurring quarterly, the DI uses the Trend Indicator to rank the ETFs in the DI’s pool of potential purchase candidates. Only the ETFs with the strongest upward price trend are bought and held until the next Review event when the process is repeated. Thus, all trade decisions are made based on objective observations of easy to find market data and not on risk-laden subjective human judgments or complex computer algorithms. DIs were designed to be so simple that individuals of virtually all experience levels can implement and manage them on their own, if they wish, using an online broker.

How DIs Capture Market Gains

The following series of charts and a table illustrate how Dynamic Investments work and how they performed during the volatile market period from the start of 2007 to August of 2018 when these words were written.

Stock / Bond Performance 2007 - 2018

The first chart, just below, shows the value growth of a total market Stock ETF and a total market Bond ETF during the test period. Just below the chart is a bar that shows which of these two assets the simple NAOI "Primary" DI selected and held during this period. This is the simplest DI possible that only rotates between Stocks and Bonds based on the price trends of each. Keep in mind that all DI trade signals were generated automatically by the DI based on a periodic observation of market trend data; no human subjective decisions were involved.

You can see that the NAOI designed DI was able to automatically detect uptrends in both Stocks and Bonds and change the ETF it held to take advantage of them while avoiding the losses of downtrends. DIs are market-sensitive while MPT portfolios are not and the difference in performance is astounding as discussed next.

The Primary DI Value Growth 2007-2018

So, how did this simple DI perform? The chart just below illustrates that it performed extremely well. It shows the value growth of the DI during the test period. For comparison purposes, it also shows, at the bottom of the chart, the value growth of an industry standard MPT portfolio with a 60% allocation to Stocks and a 40% allocation to Bonds. You can see that the DI increased in value during this period by 1765% while the MPT portfolio increased by only 91%. And, again, keep in mind that this performance was achieved based on the use of objective data, not on subjective human judgments that would inject a massive risk element into the process!

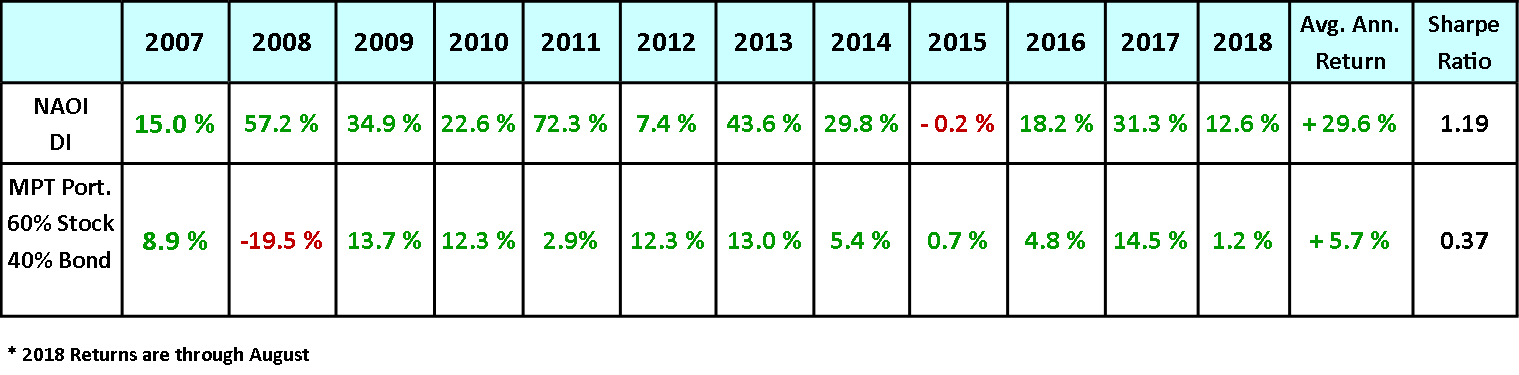

Primary DI Returns 2007-2018

Now let's transform the data in the above chart to return and risk numbers. The table below shows the annual returns for both the DI and the MPT portfolio along with the Average Annual Return and Sharpe Ratio for each. The Sharpe Ratio measures the amount of risk received for each unit of risk taken, the higher the better. And any value greater than 1.0 indicates a superior investment.

Today's financial experts will say that returns like those produced by the DI are impossible. And they ARE impossible using MPT methods. But once the constraints of MPT are lifted, returns are allowed to soar without increased risk.

How Are Returns Like This Possible?

To explain how DIs produce such exceptional returns let's think about the differences between DIs and MPT portfolios. First, a DI strives to hold ONLY ETFs that are moving up in price. MPT portfolios are designed to hold both winning and losing investments at all times and thus severely limiting their returns. DIs are capable of changing the ETF they hold based on a periodic sampling of market trends. MPT portfolios are static and blind to market movements. As a third difference, DI trades are made based on objective observations of market data while MPT portfolios only change based on human judgments that inject a massive risk element into the trade decision process.

New Concepts In Investing

When DIT replaces MPT the world of investing changes at a fundamental level and outcomes seen as impossible today suddenly become real. This is because DIT is not a variation of MPT, it is a totally new approach to investing. Here are just few new concepts that DIT introduces into the investing process:

Time-Diversity - This is a new portfolio diversity element that does not exist in the MPT world. Time-diversity arises from the fact that DI's automatically signal changes to their holdings over time based on a periodic sampling of market trends. And time-diversity is unique in that it not only reduces risk but also enhances returns. Company diversity and asset diversity used by MPT reduce risk but also reduce returns. Time-diversity is a major reason that DIs produce far higher returns than static MPT portfolios.

Objective Decision Making - A major problem in the world of investing today is the almost universal use of human subjective judgments to make trade decisions. Such judgments can be adversely affected by emotions, bad data, faulty analysis, sales bias and even outright fraudulent activities. DIs eliminate this major risk factor by basing all trade decisions on the objective observation of empirical market trend data. Reducing or eliminating the human risk factor is essential for enabling the field of investing to meet the needs of the investing public.

Higher Returns without Higher Risk - This new investing concept is a stunner. MPT says that higher returns can only be achieved by assuming higher risk. If this isn't true the entire MPT theory crumbles. Well, DIT shows that it isn't true as illustrated in the returns table just above where the DI produced higher returns with lower risk than an MPT portfolio using the same ETFs over the same time period. Using DIs, higher returns without higher risk can also be produced by simply placing more ETFs in the Dynamic ETF Pool and giving the DI more areas of the market to search for uptrends. When the risk-return link is severed, the world of investing changes at a fundamental level! That's exactly what has happened with the introduction of DIs.

These are just three major new concepts of investing made possible by DIT that don't exist in an investing world based on MPT.

The Productization of Investing!

Another massive benefit of using DIs is that they productize the world of investing. This is perhaps one of the most significant advances in the world of investing since MPT was introduced in 1952. When portfolios become standardized consumer products the entire industry changes - for the better. Let's briefly discuss what makes Dynamic Investments "portfolio products".

- All DIs have the universal goal of capturing positive returns wherever and when ever they occur in the market. There is no need to customize portfolios to match each investor's risk profile.

- Each DI is a comprehensive, intelligent and self-managing investment. It specifies the ETFs to work with as well as how they are to be traded on an ongoing basis.

- Once a DI is created, its design does not change even though the ETF it holds at any one time does. This is an active investment that is passively managed and the active/passive management debate goes away. DIs combine the best of both methods.

- Investors simply buy and hold DIs as their internal intelligence automatically signals trades based on objective observations of market trends. Investors don't need to worry about economic, market or world events. All of these factors are "baked-in" to market price trends.

- DI developers and providers can mass-market the Dynamic Investments they create to the industry AND directly to the public via catalogs or on their Web sites. Investors can then simply buy and implement those that meet their investing needs. They can also combine DIs in dynamic portfolios if they wish.

The "Productization of Investing" is the Holy Grail of the financial world that experts have been seeking for decades. They haven't found it. With the discovery, development and release of Dynamic Investment Theory and Dynamic Investments, the NAOI has. Make no mistake, this is a new world of investing.

Now let's ask a few questions.

Has Anyone Thought of this Approach Before?

Yes, several financial organizations have recognized that trend following is a valid and effective approach to investing. They offer products with labels such as Momentum ETFs and Smart Portfolios that use a trend-based strategy. But none offer this approach in a manner that is as simple, as reliable or as profitable as the NAOI. Plus, while other organizations simply offer trend-based "products' meant to be used in an MPT portfolio format, the NAOI offers an entire trend-based theory that rivals MPT and a comprehensive approach to investing based on it. This is a theory and rule-set that enables anyone, with NAOI training, to create powerful Dynamic Investments on their own that can outperform virtually any MPT portfolio - using the same ETFs and for the same period of time. The NAOI takes the trend following strategy to a whole different level - one that changes the very foundations of how investing works.

What Do the Skeptics Say?

I’ve heard numerous reasons why DIs cannot possibly work and none are convincing. The most frequent issue is the tax penalty related to frequent trading. In response I show that even after short-term capital gains taxes are deducted from DI returns they still provide profits that are multiple times higher than virtually any buy-and-hold, MPT portfolio. Also, most retail investing these days is done in retirement/tax-deferred accounts where short term capital gains don’t apply. The next objection I hear is that people can’t “time the market” with success. I agree, people can’t. But DIT doesn’t ask them to. DIs work based on the observation that market trends can reliably predict future price movements in at least the short term. People also suggest that this must be a trading system that will work for a short time and then stop. My response is that DIT will work as long as asset and market prices are cyclical. No amount of “over-use” will eliminate that dynamic.

Skepticism is good and I welcome it. But when offering it, give me a chance to respond. I have spend 5+ years studying and developing DIT and Dynamic Investments. I truly believe that any objection can either be discounted or remedied.

A Boon for the Financial Services Industry

The financial services industry should not view DIT and DIs as a threat but rather as a gateway to a vast new world of opportunities and profits. Because DIs meet the goals of the investing public, they will entice millions of potential clients to enter the market. These are people who are now not active investors because of the uncertainty and risk they see as being inherent in the markets and the ineffective use of MPT-based portfolios. The high returns and risk reduction elements of DIs mitigate the fears of the public and new clients will flood the market to buy them. For this reason alone the industry should embrace DIT. But there are other reasons as well.

New, powerful DIs are easy to create, bypassing the time, cost and effort of developing new ETFs or mutual funds. They are formed by simply combining existing ETFs, mutual funds, or other liquid investment vehicles in the DI structure. As a result, investment product developers and advisors will be able to expand their product lines virtually overnight and offer dynamic portfolios that perform far better than the MPT portfolios used today. By simply combining existing ETF combinations to create new products, developers uncover a vast reservoir of hidden value that is currently lying dormant and hidden in an ETF-only product line.

For financial advisors, portfolio designers and virtually anyone who recommends investments to the public, the introduction of DIT and DIs opens the door to better products, new revenue streams, increased market share and expanded product lines. This new approach gives to those that offer it a massive competitive advantage in a crowded field. And those that take advantage of it first will profit the most!

Change Is Not Optional

At this point you may be asking yourself "If this approach is so superior to MPT, why hasn't the financial services industry already adopted it?". I believe that one of the main reasons is that the financial industry is thriving now using current MPT methods, so why rock the money boat? MPT techniques are so rife with human subjective judgments that the public sees little option put to use financial advisors to navigate the world of investing today. This makes individual investors dependent on the industry and this is good for business. In contrast, DIT is so easy to understand and DIs are so simple for individuals to create, implement and manage on their own that very soon they will have the option of bypassing advisors altogether. And this would be disastrous formany multi-billion dollar business models.

But as the public learns about the simplicity, higher returns and lower risk of DIs, they will demand them. Financial organizations that meet this demand will thrive while those that don't will fade away. That's just how evolution works.

The future of investing will be determined by the investing public, i.e. the customer, not by the CEO's of financial organization or the research labs of academia. Previously the public has not had the tools to exert this power. With DIT and DIs, now they do. And, as a result, change will not be optional for the financial services industry to continue to thrive.

NAOI Support Resources

To enable financial organizations to take full advantage of the coming Dynamic Investment revolution, the NAOI offers a full range of support services including DI education seminars, DI design classes, and customized consulting services. In addition we have published a book called "The Amazing Future of Investing" that documents our research effort and shows how DIs can be used immediately to take advantage of current market dynamics. The book can be purchased in the NAOI Store (see cover below, right).

We also welcome R&D partnerships and cooperative efforts aimed at developing new methods and applications within the DIT framework. Interested parties can contact me at LHevner@naoi.org.

Web Site Road-Map

Click to go to naoi store

Of course there is much more to learn about how DIs than can be presented on this page. In fact, we have created a totally separate site dedicated to Dynamic Investment Theory at www.DITheory.com. Following are just a few pages that you may want to access next before reading the entire site.

- The DI Research and User Book / Report - "The Amazing Future of Investing" (click cover at right)

- DI Products and Dynamic Portfolios (click here)

- DI Applications for professionals (click here)

- NAOI Consulting (click here)

- NAOI DI Education Seminars and DI Design Classes (click here)

- A Word to Skeptics (click here)

- Contact the NAOI (click here)

For Immediate Updates

Consider signing-up for NAOI Email Updates at the bottom of this page to be alerted when Dynamic Investment developments occur.

"the future of investing starts here" is a registered service market of Leland Hevner and the national association of online investors